Living on the San Francisco Peninsula offers unmatched access to opportunity—world-class employers, top-tier schools, and vibrant communities. But that lifestyle comes at a cost, and for many homeowners, the monthly mortgage can feel like a second job.

The good news? There’s a practical, increasingly popular way to take control of those payments. Across the Peninsula, homeowners are rethinking how their properties work for them.

Instead of viewing a backyard as unused space, they’re transforming it into a reliable income stream. Accessory Dwelling Units (ADUs)—whether detached cottages, garage conversions, or above-garage apartments—are turning into powerful financial tools.

This isn’t just about earning a little extra rent. It’s about creating a strategy that fundamentally reshapes your financial future. By generating consistent income and applying it directly to your loan, you can reduce your out-of-pocket costs and even shave decades off your mortgage timeline.

That’s the essence of a Peninsula ADU mortgage payoff approach—using real estate intelligently to offset mortgage with secondary unit Bay Area and gain control over your Peninsula mortgage.

What Is a Peninsula ADU Mortgage Payoff Strategy

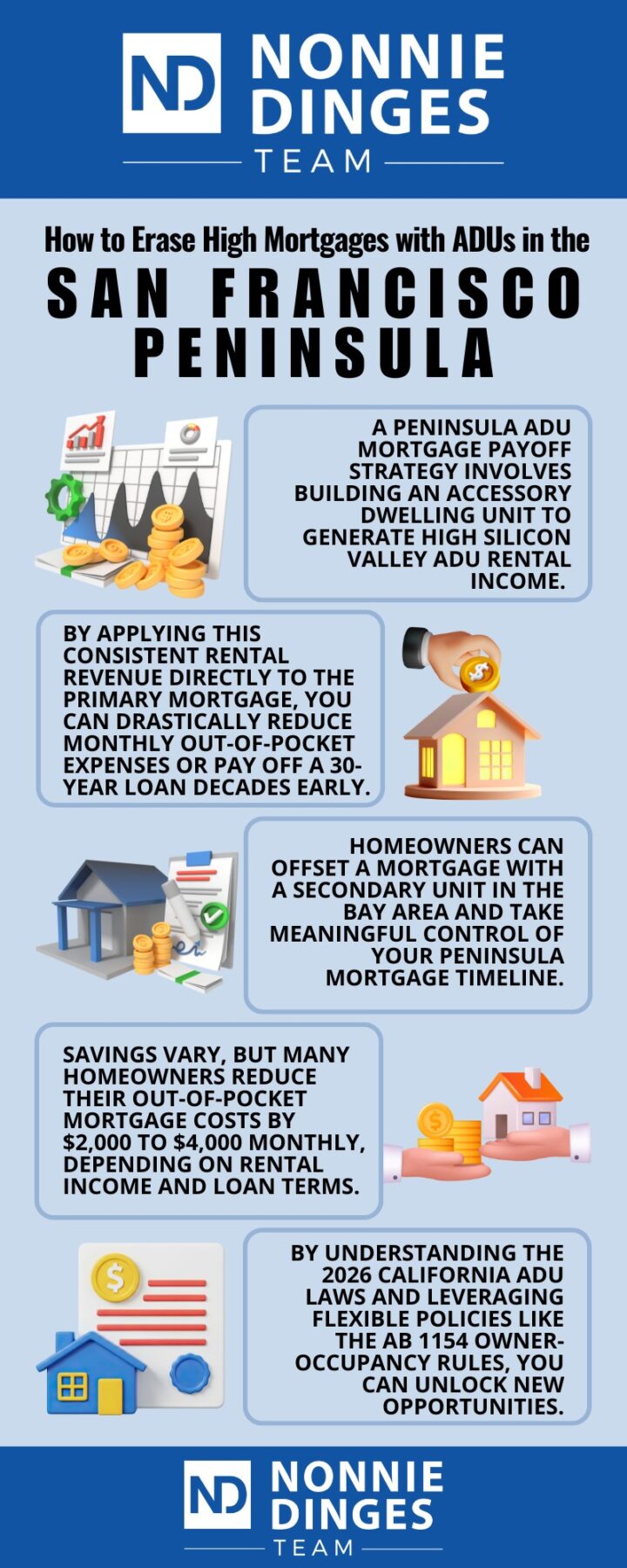

A peninsula ADU mortgage payoff strategy involves building an accessory dwelling unit to generate high Silicon Valley ADU rental income. By applying this consistent rental revenue directly to your primary peninsula mortgage, homeowners can drastically reduce their monthly out-of-pocket expenses or pay off their 30-year loan decades early.

Navigating 2026 California ADU Laws and Regulations

Streamlined Approvals

California has made it significantly easier to build ADUs in recent years, and the 2026 California ADU laws continue that trend. The state has limited the ability of local jurisdictions to deny compliant projects, which means fewer roadblocks for homeowners.

If your plans meet zoning, size, and safety requirements, cities are generally required to approve them within a defined timeline. This has removed much of the uncertainty that used to discourage homeowners from pursuing ADU construction.

Owner-Occupancy Flexibility

Another key factor is the evolution of the AB 1154 owner-occupancy rules. These regulations prevent cities from imposing strict requirements that force owners to live on the property in order to rent out an ADU.

This flexibility opens the door for a broader range of uses. Whether you live in the main home and rent the ADU—or eventually rent both units—you maintain control over how your property generates income.

Budgeting for Construction and Palo Alto ADU Permit Fees 2026

The Initial Investment

Let’s be candid—building an ADU isn’t cheap. Costs vary widely depending on size, design, and location, but homeowners should expect to invest significantly upfront.

Beyond construction and labor, you’ll need to account for local administrative costs, including Palo Alto ADU permit fees 2026. These can differ from city to city across the Peninsula, sometimes by tens of thousands of dollars.

The key is planning thoroughly. A well-structured budget ensures that your project doesn’t stall midway and that your expected return remains intact.

Maximizing Your Space

Design matters more than many homeowners realize. A thoughtfully designed ADU—modern finishes, efficient layout, good natural light—can command higher rent and attract better tenants.

In a competitive rental market like the Peninsula, small details translate directly into higher monthly income and faster returns on your investment.

Financing Your Build with Construction-to-Permanent Loans in California

Funding the Project

Utilizing construction-to-permanent loans in California allows homeowners to finance the ADU build and then seamlessly roll that cost into a single, permanent loan once the unit receives its certificate of occupancy.

This approach simplifies the financing process. Instead of juggling multiple loans, you transition from construction financing into a long-term mortgage with predictable payments.

Leveraging Future Income

One of the most exciting developments in lending is the ability to use projected rental income to qualify. Many lenders now recognize the earning potential of ADUs and factor that into your borrowing capacity.

This means your future rental income can help you secure financing today—making it easier to move forward with your project without overextending yourself financially.

Maximizing Silicon Valley ADU Rental Income

The Tenant Pool

Demand for housing on the Peninsula remains incredibly strong. From tech professionals to traveling nurses and graduate students, there’s a steady stream of renters looking for high-quality, private living spaces.

That demand drives impressive Silicon Valley ADU rental income, often ranging from $2,000 to $4,000+ per month for a well-designed one-bedroom unit, depending on location.

For many homeowners, that’s enough to cover a substantial portion—sometimes more than half—of their monthly mortgage payment.

Property Value Appreciation

Beyond monthly cash flow, adding an ADU enhances your property’s overall value. Buyers increasingly view ADUs as desirable features, especially in high-cost markets.

So while you’re using rental income to offset your mortgage today, you’re also building long-term equity that pays off when it’s time to sell.

Financial Strategy Comparison Table

| Financial Factor | Standard Peninsula Mortgage | With ADU Rental Offset |

|---|---|---|

| Monthly Out-of-Pocket | Very High | Significantly Reduced |

| Property Value | Base Market Value | Base Value + ADU Premium |

| Loan Payoff Speed | Standard 30 Years | Accelerated |

| Maintenance Responsibility | Primary Home Only | Primary Home + Rental Unit |

Key Takeaway

High housing costs don’t have to define your financial future. With the right approach, your property can become a powerful wealth-building tool.

By understanding the 2026 California ADU laws and leveraging flexible policies like the AB 1154 owner-occupancy rules, you can unlock new opportunities.

Careful budgeting—including localized costs like Palo Alto ADU permit fees in 2026—combined with smart financing options such as construction-to-permanent loans in California, positions you to succeed.

Add in strong Silicon Valley ADU rental income, and you have a strategy that doesn’t just ease your monthly burden—it accelerates your path to financial freedom.

This is the true power of a Peninsula ADU mortgage payoff strategy: the ability to offset mortgage with secondary unit Bay Area and take meaningful control of your Peninsula mortgage timeline.

If you’re considering building an ADU or want to understand how this strategy could work for your specific property, it helps to talk it through with someone who knows the Peninsula market inside and out.

Every lot, zoning rule, and financing profile is different—and having a clear plan can make all the difference.

Reach out directly at 650-218-3353 or email dingesnonnie@gmail.com to start the conversation.

Whether you’re just exploring ideas or ready to take the next step, you’ll get straightforward guidance tailored to your goals—and a clear path toward turning your backyard into a true financial asset.

Frequently Asked Questions

Savings vary, but many homeowners reduce their out-of-pocket mortgage costs by $2,000 to $4,000 monthly, depending on rental income and loan terms.

In many cases, parking requirements have been relaxed or eliminated, especially for properties near public transit or in urban areas.

Generally, yes—Palo Alto tends to have higher fees, though exact costs depend on project specifics and city policies.

They provide flexibility by limiting strict occupancy requirements, allowing more freedom in how you use and rent your property.

Yes. Many homeowners tap into home equity through refinancing or HELOCs to fund ADU construction.

Typically between $2,000 and $4,000+ per month, depending on location, amenities, and design quality.

Not usually. Most homeowners incorporate the ADU cost into their existing mortgage or a new consolidated loan.